SPACgetti: From SNII to RGTI

Rigetti Inc goes public, but did they raise enough money?

What follows is not financial advice, it is for entertainment only, etc, etc. I have no position in $RGTI.

Update 03/02/2022: I had the chance to confer with some fabrication experts and discovered I was off base on the fabrication constraints Rigetti is likely to face. I have made the appropriate edits below.

With the Russian invasion of Ukraine starting last week, I’ve been a little distracted from developments in quantum computing. However, since my geopolitics takes are sequestered on my other blog1, it’s time to engage in our favorite traditional activity: writing another SPAC post.

As you may recall, Rigetti Inc announced their SPAC in early October 2021. If you’d like a refresher, you can take a look at my previous post on the subject.

Since then we have waited while the gears of Business turned, culminating in an announcement of a successful vote to merge from the shareholders of $SNII. Some quotes from the press release (bolding is mine):

Supernova reported that all of the various proposals giving effect to the previously announced business combination between Supernova and Rigetti Holdings, Inc. ("Rigetti" or the "Company") were approved by approximately 95% of the shares of Supernova voted at the extraordinary general meeting. A Form 8-K disclosing the full voting results will be filed with the Securities and Exchange Commission on February 28, 2022.

Additionally, the deadline for electing redemptions has passed and Supernova will have approximately $114 million in its trust account prior to the business combination. Rigetti will receive gross proceeds of $261.75 million from the transaction, which includes $147.51 from a fully committed PIPE.

The good news: Rigetti Inc is definitely going to be a public company! The bad news: the redemptions are such that they will only be receiving ~$262 million of a maximum $450 million in funding, or about 58% of value if they’d had no redemptions. My understanding of the situation is that Supernova held $345 million in trust, pending the redemption deadline, of which $114 million will remain. So it would seem that roughly 67% of shareholders elected to redeem their shares for cash rather than continue to hold shares past the merge.

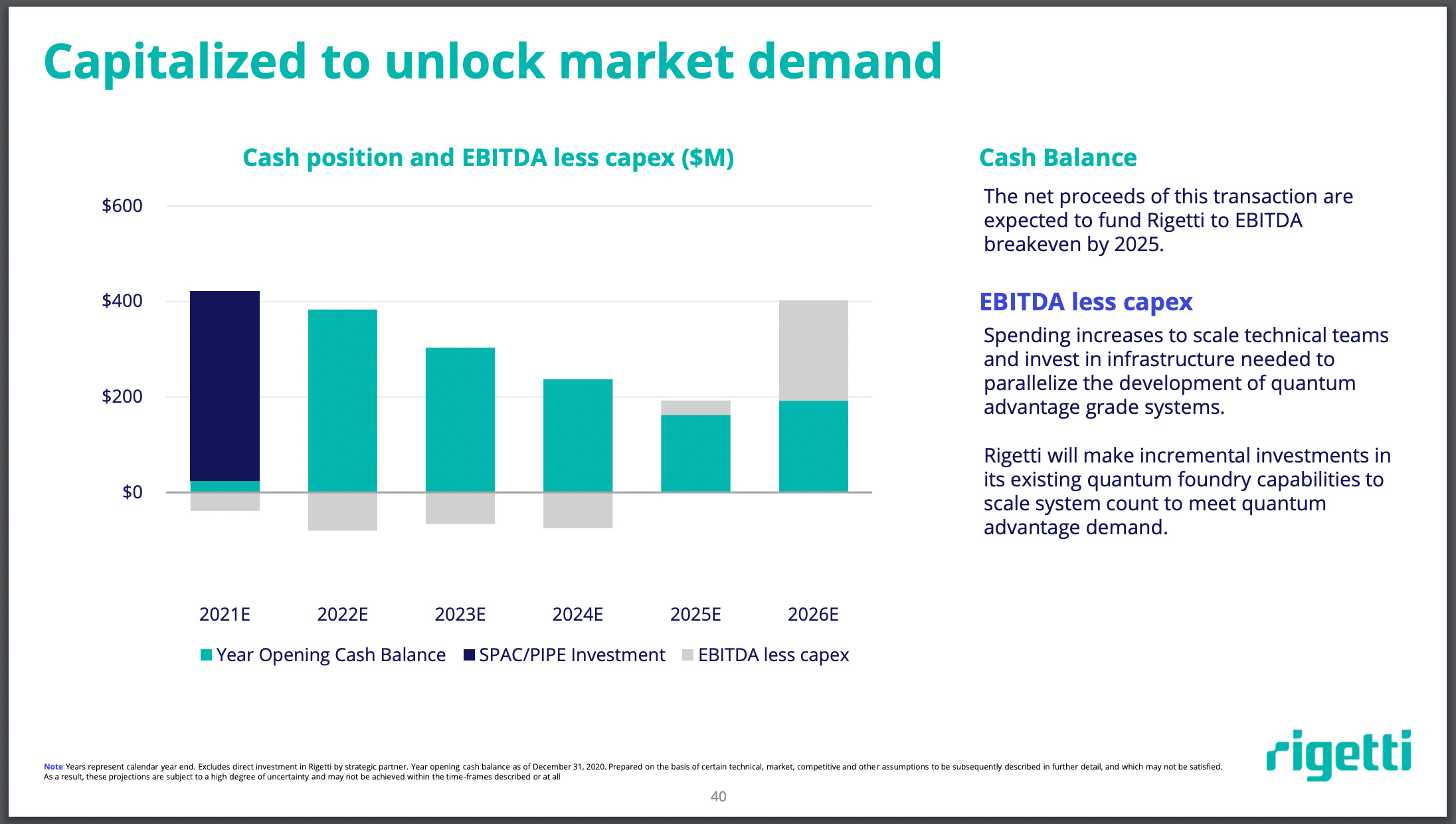

Let’s take a look at how this situation compares to the more optimistic outlook from the original Rigetti investor presentation. Note that this slide doesn’t exist in the updated January investor presentation.

Based on this optimistic view, Rigetti expects to hit breakeven by the end of 2025, and positive cash flow by 2026, roughly 4-5 years from now. Additionally, they expect to spend something like $200-$300 million in pursuit of this goal. With the full SPAC funding, that would leave them with a cushion of about $175 million in cash at the end of 2025.

With the actual SPAC funding amount, $265 million, this leaves them with more or less $0 by the end of 20252. Honestly, the situation seems grim. I would assume that the chart above is an optimistic case, since we all know everything in science takes about 50 - 500% longer than you think or hope it will. And indeed, a $450 million cash balance would have given Rigetti some leeway to reach profitability. Possibly out to 2028, if they can hold their burn rate to ~$60 million per year, as per the chart.

At the end of the road there are a few options that I can see:

Rigetti is profitable and everything is fine.

Rigetti runs out of cash and issues debt3 to raise more money.

Rigetti runs out of cash and gets acquired by a larger player in QC, or a non-QC company that wants to enter the field.

Rigetti runs out of cash and shuts down, liquidating itself.

I don’t have much to say about Option 1, it’s pretty self-explanatory, and would suggest an amazing business environment for (superconducting) quantum computing companies.

Option 2 is interesting, but it seems unlikely. Who would buy the debt of a broke deep-tech company whose tech isn’t ready?

Option 3 could make sense for a non-QC company. I am not sure what value say, Google or IBM would see in Rigetti’s IP, since both Google and IBM have chosen their architectures. On the other hand, the lead times for buying a dil fridge are pretty substantial, so it could be worth it to get a bunch of operational fridges and people qualified to run them fairly quickly.

Option 4 is also pretty self-explanatory and not very interesting.

Obviously, Rigetti is shooting for Option 1, but being bought out (Option 3) might not be so bad either. We’ve already estimated that there are about 4 years available, so what can they do in that time?

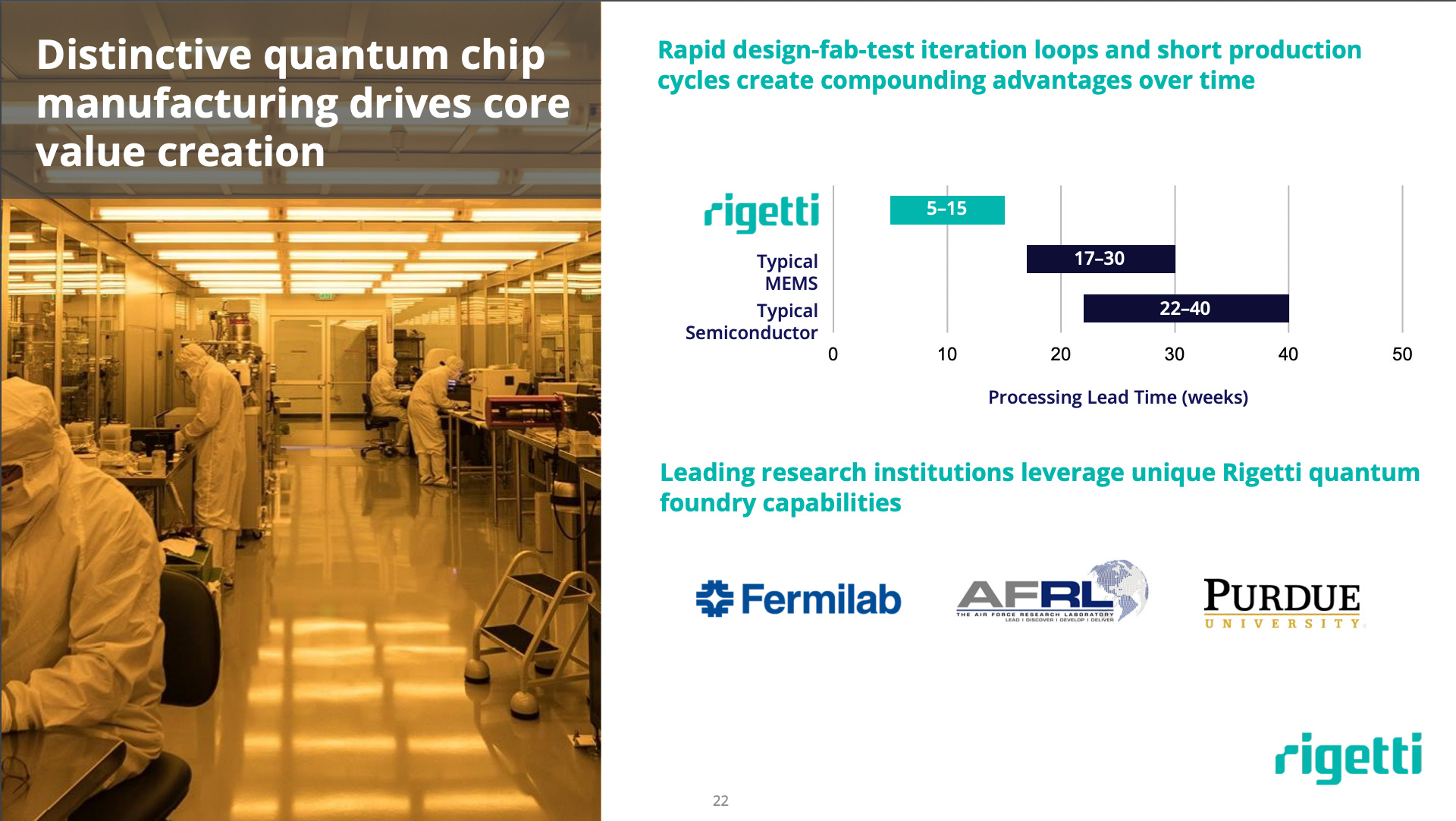

According to the investor presentation, Rigetti chip fabrication lead times are about 5-15 weeks.

Let’s pretend that, even as the complexity of Rigetti QPUs scales up, they’re able to hold their fab times to a 15 week maximum, per mask. How many fab cycles can they run in 4 years? This actually depends on how many masks they can process at once. If it’s one mask at a time, then they can run 13 fab cycles if each one takes 15 weeks. Without any specific knowledge of the Rigetti foundry, we might guess that their fab can do 3 masks simultaneously. One mask is starting, one mask is half way through, and one almost complete, which gets us to 39 overlapping 15-week fab cycles4.

I learned that pro-tier fabs can start many, many wafers per day, so fab cycles is not the real constraint that Rigetti will face. My fab friends speculate that a fab worth a few hundred million dollars, could be a single-stream fab, with little or no tool redundancy. So if one tool goes down, for any reason, the whole production line is halted. This, obviously, is ameliorated by having multiple streams, or at least multiples of the fab tools most likely to break. I suspect that most/all fabrication tools are very long lead items, especially given the recent global difficulties with supply chains. That, combined with the gigantic price tags some of these things carry, means that any near-term improvements to the Rigetti fab are likely already bought and paid for.

Given that it’s likely that the Rigetti Fab 1 facility can start wafer basically as fast as the design team can deliver them, the design team could be driven pretty hard to deliver many iterations and improvements ASAP. Of course, this kind of rapid chip design and fab effort is pretty punishing on a design team, unless there are 2-3 sub-teams so that each set of designers has a full 5-15 weeks to lay out the next iteration of chips. The internet claims that Rigetti has 145 employees, so it’s certainly possible that they have enough staffing to meet this challenge.

Unfortunately, a major constraint in the design-fab process is the actual test of new chips5. In my experience, the only way for the design and fabrication teams to get any reliable feedback is through the test team in the lab. Even a well-run, productive lab will be subject to major unforeseen issues. Dilution refrigerators alone are finicky beasts and any number of problems can take a fridge down for weeks or months. Chips might have systemic issues, there could be design mistakes that make them difficult to test, wear and tear inside the fridge could cause signal integrity issues that are only spotted at milliKelvin temperatures, to name a few. Hell, the IBM 127 qubit chip (Washington) has been ‘online’ for months and still has CNOT calibration errors at exactly 100% for some qubit pairs.

The point is that the test team must acquire meaningful data to feed back to the design teams before the next set of chip designs is out the door or risk an ‘open loop’ design cycle, where changes are made mostly blind, or from incomplete data. An open loop could risk an entire fab run being worthless for mostly preventable reasons, versus the usual unpredictable calamities that can afflict superconducting device fabrication. Remember, if we’re overlapping 3 masks at a time, there are only 39 such 15 week cycles in 4 years.

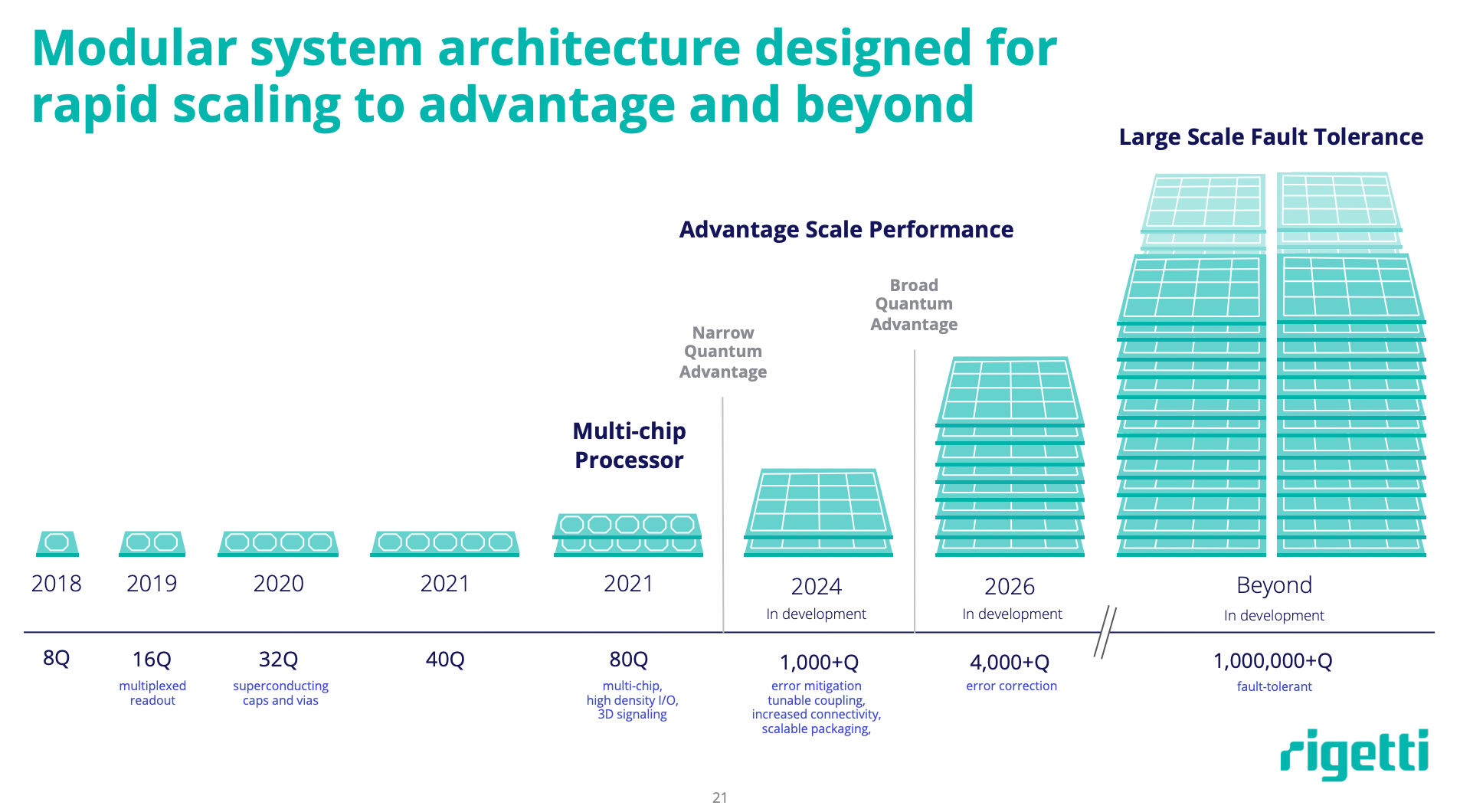

And as you can see above, the Rigetti roadmap is extremely aggressive. 1000 qubits by 2024, 4000+ by 2026. Additionally, we have some clues about what the design and test teams have to have cracked by 2025: error mitigation, tunable coupling, increased connectivity, scalable packaging. Also at the same time, the number of qubits must increase by > 10x. Oh yeah, and Rigetti has partnerships and cloud-accessible QPUs to maintain, so does that mean some amount of their 14 systems6 are simply unavailable to the R&D effort?

To me situation seems bleak. There are real, physical constraints to how fast Rigetti can iterate here, and mistakes can cost weeks or months. Rigetti is not in a world where errors can be reverted to the last good commit. Errors in fabrication are indelible, they can’t be erased or reverted. Leaks in dilution units and faulty cables must be painstakingly tracked down and fixed, if there are spare parts available. Measured in seconds, hours or days, 4 years can seem like a long time. Measured in fab cycles, fridge cooldowns, or experimental timelines, 4 years is more like the blink of an eye. Certainly, if the Rigetti team wants a miracle, they’re gonna have to build one.

Sorry, there is no other blog. You’ll just have to text me for hot takes.

To within a few million dollars.

I don’t really know how this works, so if actual Business People have insight as to how this could possibly go down, I’d be interested to hear it.

In reality, they likely do many short 5 week cycles between 15 week cycles. The long cycles would be major revisions to flagship architectures, while the short loops focus on identifying and ameliorating specific deficiencies. This still requires a pretty fast paced design effort and can still be vulnerable to open loop effects on individual masks. And, of course, there’s always the possibility that there are some problems that can only be discovered with the fully integrated devices, rather than on targeted short-loop chips.

This is the realest constraint, in my opinion.

See slide 30 of the January Investor Slides

I enjoy your articles and would like to get to know you better. Is there a way to reach you?

I happen to think that their recent partnership with Riverlane is potentially important. Thus far I'm probably most bullish on PsiQuantum.